ประเภทของบริษัทโฮลดิ้ง

เมื่อต้องจัด “โครงสร้างบริษัท” โฮลดิ้งครอบครัว สิ่งแรกคือต้องเข้าใจประเภทต่างๆ ของบริษัทโฮลดิ้งที่สามารถจัดตั้งได้ แต่ละประเภทมีก็จะวัตถุประสงค์ที่แตกต่างกัน ซึ่งจะมีลักษณะเฉพาะตัวของแต่ละแบบ

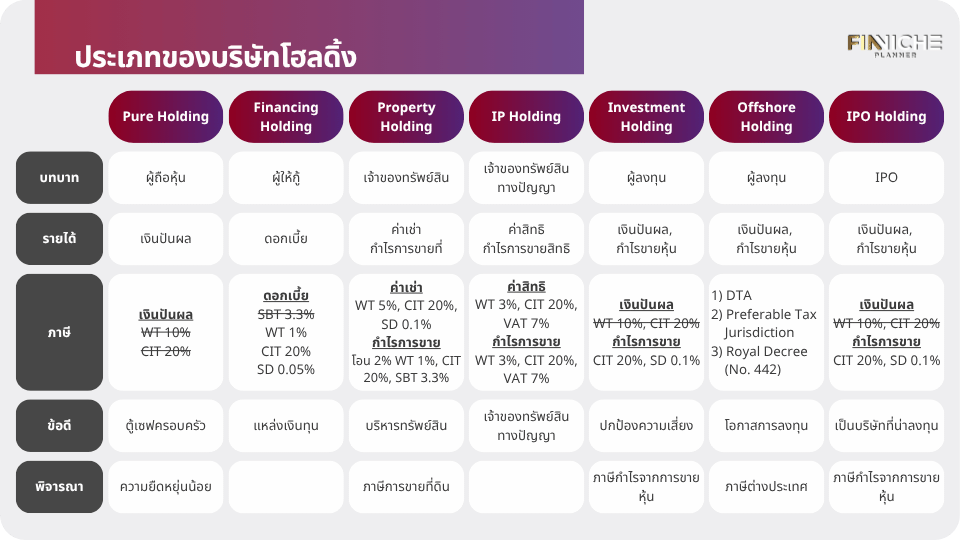

“โครงสร้างบริษัท” แบบ Pure Holding Company

บริษัทโฮลดิ้งประเภทนี้มีอยู่เพื่อถือหุ้นในบริษัทอื่นเท่านั้น ไม่ได้ประกอบธุรกิจหรือกิจการใดๆ โดยทั่วไปจะเป็นบริษัทจัดตั้งใหม่เพื่อหน้าที่เดียวเท่านั้น คือการรวมความเป็นเจ้าของและการควบคุมบริษัทในเครือเข้าด้วยกัน ทำให้ “โครงสร้างบริษัท” ประเภทนี้จะมีรายได้ทางเดียวคือรายได้จากเงินปันผล ทำให้เหมาะสำหรับครอบครัวที่ต้องรวมการตัดสินใจและการจัดการไว้ที่ศูนย์กลาง

- บทบาท : เป็นผู้ถือหุ้นของบริษัทในเครือ

- รายได้ : เงินปันผล

- ภาษี : เมื่อตั้งบริษัทตามเงื่อนไขในมาตรา 65 ทวิ (10) แห่งประมวลรัษฎากร จะได้รับการยกเว้นภาษีหัก ณ ที่จ่าย 10% จากรายได้เงินปันผล และยกเว้นภาษีเงินได้นิติบุคคล 20% จากรายได้เงินปันผล

- ข้อดี : เป็นแหล่งเก็บเงินทุนของธุรกิจครอบครัวซึ่งได้รับสิทธิประโยชน์ทางภาษีด้วย นอกจากนั้นยังเป็นเครื่องมือในการรวมศูนย์ สร้างกรอบอำนาจการบริหารเพื่อควบคุมดูแลบริษัทในเครือ

- ข้อควรพิจารณา : หลักการของบริษัทโฮลดิ้งคือการรวมศูนย์ซึ่งอาจจะทำให้ความยืดหยุ่นลดลง เช่น หากสมาชิกครอบครัวที่เป็นผู้ถือหุ้นต้องการขายหุ้นธุรกิจครอบครัวอาจติดกฎเกณฑ์ของบริษัทโฮลดิ้ง หรือการมีกรอบอำนาจทำให้ต้องจัดประชุมในบริษัทโฮลดิ้งเพื่อตัดสินใจ

“โครงสร้างบริษัท” แบบ Mixed Holding Company

บริษัทโฮลดิ้งแบบผสมถึงจะถือหุ้นในบริษัทอื่นแต่ก็ยังดำเนินการธุรกิจอื่นๆด้วย “โครงสร้างบริษัท” นี้จะช่วยให้ครอบครัวไม่เพียงแต่จัดการสินทรัพย์เท่านั้น แต่ยังดำเนินกิจกรรมทางธุรกิจโดยตรงอีกด้วย บริษัทโฮลดิ้งประเภทนี้มีความยืดหยุ่นสำหรับครอบครัวที่ต้องการควบคุมการดำเนินงานของกิจการธุรกิจบางอย่าง ในขณะที่ยังได้รับประโยชน์จากการรวบรวมและจัดการทรัพย์สินอื่นๆด้วย ซึ่งบริษัทโฮลดิ้งแบบผสมก็อาจจัดตั้งตามวัตถุประสงค์ต่างๆ ดังนี้

Financing Holding Company

- บทบาท : เป็นแหล่งเงินทุนของบริษัทในเครือ จากการรวบรวมเงินปันผลของแต่ละบริษัท

- รายได้ : ดอกเบี้ยเงินกู้จากบริษัทในเครือ

- ภาษี :

- ได้รับการยกเว้นภาษีธุรกิจเฉพาะ 3.3% เมื่อครบเงื่อนไขตามพระราชกฤษฎีกา (ฉบับที่ 571) พ.ศ. 2556 มาตรา 3

- เสียภาษีหัก ณ ที่จ่าย 1% ภาษีเงินได้นิติบุคคล 20% และอากรแสตมป์สัญญาเงินกู้ 1 บาท ทุก 2,000 บาท หรือเศษของ 2,000 บาท แห่งยอดเงินให้กู้ยืม (0.05%) ไม่เกิน 10,000 บาท

- ข้อดี : สามารถบริหารเงินทุนในองค์กรได้อย่างมีประสิทธิภาพ

Property Holding Company

- บทบาท : ถือครองที่ดินให้เช่า หรือขายทำกำไรในอนาคต

- รายได้ : รายได้ค่าเช่าที่ดิน รายได้จากการขายที่ดิน

- ภาษี :

- รายได้ค่าเช่า เสียภาษีหัก ณ ที่จ่าย 5% ภาษีเงินได้นิติบุคคล 20% และอากรแสตมป์ 1 บาท ทุก 1,000 บาท หรือเศษของ 1,000 บาท (0.1%)

- รายได้จากการขายที่ดิน มีค่าธรรมเนียมการโอน 2% และเสียภาษีหัก ณ ที่จ่าย 1% ภาษีเงินได้นิติบุคคล 20% ภาษีธุรกิจเฉพาะ 3.3%

- ข้อดี : จัดการทรัพย์กงสี (ที่ดิน) ในเรื่องของกรรมสิทธิ์รวมได้ เช่น ครอบครัวหนึ่งมีพี่น้อง 5 คน เมื่อซื้อที่ดินที่เป็นที่ดินส่วนรวม แต่บางทีก็ใส่ชื่อ 3 คนพี่น้องบ้าง 2 คนบ้าง เมื่อทำธุรกรรมผู้ที่มีชื่อต้องไปทำทุกคน ทุกคนต้องตัดสินใจเป็นเอกฉันท์ หากมีใครคัดค้านก็ไม่สามารถทำธุรกรรมได้ อีกเรื่องหนึ่งคือเมื่อมีใครคนใดคนหนึ่งเสียชีวิต ผู้รับมรดกก็จะเข้ามาเป็นกรรมสิทธิ์รวมต่อ จากเดิมเป็นกรรมสิทธิ์ 3 คนก็อาจเพิ่มเป็น 5 คน 8 คน

- ข้อควรพิจารณา : หากเป็นที่ดินที่เป็นชื่อสมาชิกในครอบครัว การนำที่ดินเข้าเป็นทรัพย์สินของบริษัทเสมือนการขาย ต้องเสียภาษีการขายที่ดิน และเมื่อบริษัทต้องการขายออกก็ต้องเสียภาษีอีกรอบ ฉะนั้นการตั้งบริษัทโฮลดิ้งเพื่อครอบครองที่ดินต้องมีการวางแผนอย่างรัดกุม และวางแผนถึงภาษี และมรดกในอนาคตด้วย

IP Holding Company (Intellectual Property)

- บทบาท : เป็นพอร์ตโฟลิโอทรัพย์สินทางปัญญาของทั้งองค์กร เพื่อการจัดการให้บริษัท สาขา หรือบุคคลภายนอกใช้ผ่านข้อตกลงของบริษัทแม่ เพื่อปกป้องผลประโยชน์ของกลุ่มและป้องกันไม่ให้ทรัพย์สินทางปัญญา “รั่วไหล” ทรัพย์สินทางปัญญา อาจหมายถึง เครื่องหมายการค้า สิทธิบัตร ลิขสิทธิ์ เป็นต้น

- รายได้ : ค่าสิทธิ กำไรเมื่อขายทรัพย์สินทางปัญญา

- ภาษี :

- ค่าสิทธิ เสียภาษีหัก ณ ที่จ่าย 3% ภาษีเงินได้นิติบุคคล 20% และภาษีมูลค่าเพิ่ม 7%

- กำไรเมื่อขายทรัพย์สินทางปัญญา เสียภาษีหัก ณ ที่จ่าย 3% ภาษีเงินได้นิติบุคคล 20% และภาษีมูลค่าเพิ่ม 7%

- ข้อดี : สามารถจัดการความเป็นเจ้าของในทรัพย์สินทางปัญญา และปกป้องทรัพย์สินทางปัญญาจากความเสี่ยงในบริษัทการค้าหรือบริษัทประกิบกิจการได้

Investment Holding Company

- บทบาท : เพื่อการลงทุนแบบร่วมลงทุน หรือลงทุนในบริษัทอื่นที่ไม่ใช่ธุรกิจครอบครัว

- รายได้ : เงินปันผลจากบริษัทร่วมทุนหรือบริษัทที่ไปลงทุน กำไรจากการขายหุ้นที่ถือ

- ภาษี :

- เงินปันผล เสียภาษีหัก ณ ที่จ่าย 10% และภาษีเงินได้นิติบุคคล 20% (เว้นแต่จะเข้าเงื่อนไขมาตรา 65 ทวิ (10) แห่งประมวลรัษฎากร จึงจะได้รับยกเว้น)

- กำไรจากการขายหุ้น เสียภาษีเงินได้นิติบุคคล 20% และอากรแสตมป์ตราสารการโอนหุ้น 1 บาท ทุก 1,000 บาท (0.1%)

- ข้อดี : เป็นตัวแทนผู้ถือหุ้นในการลงทุนกับบุคคลภายนอก ซึ่งเป็นกันชนอีกชั้นเพราะอาจมีความเสี่ยงจากการประกอบธุรกิจ หรือการฟ้องร้อง

Offshore Holding Company

- บทบาท : บทบาทคล้าย Investment Holding Company แต่มีจุดประสงค์ในการลงทุนที่ต่างประเทศ

- รายได้ : เงินปันผลจากบริษัทร่วมทุนต่างประเทศ กำไรจากการขายหุ้นที่ถือ

- ภาษี :

- บริษัทโฮลดิ้งจัดตั้งที่ต่างประเทศและลงทุนในต่างประเทศ หากจัดตั้งในประเทศที่ได้ประโยชน์ทางภาษี หรือทำอนุสัญญาภาษีซ้อนกับไทย (DTA: Double Tax Agreement) บริษัทโฮลดิ้งไม่เสียภาษีเงินปันผล และไม่เสียภาษีกำไรจากการขายหุ้น

- บริษัทโฮลดิ้งจัดตั้งในประเทศไทศไทยแต่ลงทุนในต่างประเทศ เงินได้รับยกเว้นภาษีไทยหากเข้าเงื่อนไขในพระราชกฤษฎีกาฯ (ฉบับที่ 442) พ.ศ.2548 ตามมาตรา 5 วีสติ

- บริษัทถือหุ้นในบริษัทผู้จ่ายเงินปันผลไม่น้อยกว่า 25% ของหุ้นทั้งหมดที่มีสิทธิออกเสียง เป็นระยะเวลาไม่น้อยกว่า 6 เดือน นับแต่วันที่ได้หุ้นนั้นมาจนถึงวันที่ได้รับเงินปันผล และ

- เงินปันผลต้องมาจากกำไรสุทธิที่มีการเสียภาษีในประเทศของบริษัทผู้จ่ายเงินปันผล โดยอัตราภาษีดังกล่าวต้องไม่ต่ำกว่า 15% ของกำไรสุทธิ ทั้งนี้ ไม่ว่าประเทศของบริษัทผู้จ่ายเงินปันผลจะมีกฎหมายลดหรือยกเว้นภาษีสำหรับกำไรสุทธิให้แก่บริษัทนั้นหรือไม่ก็ตาม

- การยกเว้นภาษีนี้ใช้สำหรับบริษัทที่ประกอบกิจการ แต่ถ้าเป็นบริษัทโฮลดิ้งที่ไม่เสียภาษีในประเทศนั้นๆอยู่แล้ว การจ่ายปันผลกลับมาที่บริษัทโฮลดิ้งในไทย บริษัทจะต้องนำมารวมเป็นรายได้เพื่อเสียภาษีเงินได้นิติบุคคล 20%

- ข้อดี : สามารถเพิ่มศักยภาพให้กับธุรกิจ โดยการขยายการลงทุนในต่างประเทศ

- ข้อควรพิจารณา : เงินปันผลของผู้ถือหุ้นในฐานะบุคคลธรรมดาที่เกิดขึ้นในต่างประเทศ หากนำเข้ามาในไทยต้องนำมารวมเสียภาษีบุคคลธรรมดา

IPO Holding Company

- บทบาท : บทบาทคล้าย Investment Holding Company แต่มีจุดประสงค์เพื่อเข้าตลาดหลักทรัพย์โดยการรวมบริษัทในเครือเพื่อเป็น “กลุ่มบริษัท”

- รายได้ : เงินปันผล กำไรจากการขายหุ้น

- ภาษี :

- เงินปันผลที่ได้รับจากบริษัทในเครือไม่เสียภาษีหัก ณ ที่จ่าย 10% และภาษีเงินได้นิติบุคคล

- กำไรจากการขายหุ้น เสียภาษีเงินได้นิติบุคคล 20% และอากรแสตมป์ตราสารการโอนหุ้น 1 บาท ทุก 1,000 บาท (0.1%)

- ข้อดี : ทำให้เป็นบริษัทที่น่าสนใจในตลาดทั้งด้วยงบการเงินที่แข็งแกร่ง (Consolidated Financial Statements) และธุรกิจที่มีความหลากหลาย (Business Diversification)

- ข้อควรพิจารณา : เมื่อบริษัทโฮลดิ้งขายหุ้นและมีกำไร จะเสียภาษีเงินได้นิติบุคคล 20% ต่างจากผู้ถือหุ้นที่เป็นบุคคลธรรมดาที่จะได้รับการยกเว้นภาษีกำไรการขายหุ้น (Capital Gain Tax)

Types of Holding Companies

When structuring a family holding company, the first thing to do is to understand the different types of Holding Companies that have a different purpose and unique characteristics.

Pure Holding Company

Pure Holding Company exists solely to hold shares of other companies and does not engage in any business activities. Typically, it is a newly formed entity with one primary goal: consolidating ownership and control of affiliated companies. Therefore, its only source of income is dividend payments. As a result, this type of holding company is ideal for families looking to centralize decision-making and management.

- Role: Shareholder of affiliated companies

- Revenue : Dividend

- Tax : When a company has met the conditions in Section 65 bis (10) of the Revenue Code, it will be exempted from 10% withholding tax and exempted from 20% corporate income tax.

- Benefits : Source of capital for family businesses, which also receives tax benefits. It is also a tool for centralizing and creating a framework of management authority to control and supervise affiliated companies.

- Considerations : The principle of holding companies is centralization, which may cause less flexibility. For example, if a family member, who is a shareholder, wants to sell a family business share but cannot do it easily due to Family Holding Company rules. In other cases, complicated operations due to a framework of authority requires a meeting to be held in the Holding Company to make the specific decision.

Mixed Holding Company

A Mixed Holding Company not only holds shares in other companies but also engages in additional business activities. Moreover, this structure allows the family to manage assets effectively while directly overseeing business operations. In addition, a Mixed Holding Company offers greater flexibility, enabling it to control certain business activities while still managing other assets within the company. It may be established for the following purposes:

Financing Holding Company

- Role: Source of capital for affiliated companies from collecting dividends

- Revenue: Interest on affiliated companies loans

- Tax:

- Exempted from specific business tax of 3.3% when the conditions are met according to the Revenue Code Amendment Royal Decree (No.571) B.E. 2556, Section 3.

- Pay withholding tax of 1%, corporate income tax of 20% and stamp duty on loan agreement which is 1 Baht for every 2,000 Baht or fraction thereof of the total amount (Amount exceeding 10,000 Baht shall be payable in the amount of 10,000 Baht.)

- Benefits: Effective the organization’s funds management with tax benefit

Property Holding Company

- Role: Own land for long-term investment such as rent, lease, or sell.

- Revenue: Rental Income, Property Sales

- Tax:

- Rental Income: pay withholding tax of 5%, corporate income tax of 20% and stamp duty of 0.1%.

- Property Sales: pay withholding tax of 1%, corporate income tax of 20% and specific business tax of 3.3%

- Benefits: In cases of joint ownership, a family can effectively manage property. For instance, if a family with five siblings purchases land, joint ownership might be shared by three siblings, or two may be named on the deed. When conducting a transaction, all parties must act together and reach a unanimous decision. However, if anyone disagrees, the transaction cannot proceed. Additionally, if one of the owners passes away, their heir will assume the role of joint owner. As a result, ownership can expand from the original three people to five or even eight joint owners.

- Considerations: If the land is registered under a family member’s name, transferring it into the company’s assets is treated like a sale, and land sale tax must be paid. Additionally, when the company decides to sell the land, tax must be paid again. Therefore, setting up a Property Holding Company to own the land requires careful planning, especially regarding future taxes and inheritance.

IP Holding Company (Intellectual Property)

- Role: It is an organization’s entire intellectual property portfolio, for use by subsidiaries, branches or external parties through parent company agreements. In result, it can protect the group’s interests and prevent intellectual property “leaking”. Intellectual property may refer to trademarks, patents, copyrights, etc.

- Revenue: Royalty, License Fee, Sale of intellectual property

- Tax:

- Royalty and License Fee: pay 3% withholding tax, 20% corporate income tax, and 7% VAT

- Sale of intellectual property: pay 3% withholding tax, 20% corporate income tax, and 7% VAT

- Benefits: It can help the ownership management over intellectual property and protection of intellectual property from business risks.

Investment Holding Company

- Role: For joint venture or investment in companies other than family businesses

- Revenue: Dividends from joint ventures or investment companies, Capital gain from selling shares

- Tax:

- Dividends: if it met the conditions in Section 65 bis (10) of the Revenue Code, dividend tax will be exempted from withholding tax of 10% and from corporate income tax of 20%.

- Capital gain: pay 20% corporate income tax and 0.1% stamp duty for share purchase agreement.

- Benefits: Representing shareholders in investing with outsiders, which is another layer of buffer of exposures from business risks or lawsuits.

Offshore Holding Company

- Role: Similar to an Investment Holding Company with the purpose of investing abroad.

- Revenue: Dividends from joint ventures, Capital gain from selling shares

- Tax:

- Holding Companies are established overseas and invest overseas. If established in a Preferable Tax Jurisdiction country or has a Double Tax Agreement (DTA) with Thailand, dividend tax and capital gains tax will be exempted.

- Holding Companies established in Thailand but investing overseas, the income is exempt from Thai tax if the conditions are met (the Royal Decree (No. 442) B.E. 2548, Section 5.

- In the 6 months preceding the dividend payment, the Thai company owns not less than 25% of the voting shares of the dividend payer; and

- The foreign company (the dividend payer) pays corporate income tax not less than 15% in its home country.

- However, tax exemptions apply only to operating companies. In contrast, if a holding company is exempt from taxes in a foreign country, any dividends paid back to the company in Thailand must be included as income, resulting in a 20% corporate income tax obligation.

- Benefits: Enhancing business potential by expanding overseas investment

- Considerations: Dividends for individual shareholders received from foreign investments, if imported into Thailand, must be included in personal income tax.

IPO Holding Company

- Role: Similarly, an Investment Holding Company may be established with the purpose of pursuing an IPO on the Stock Exchange by merging subsidiaries to form a “Conglomerate”.

- Revenue: Dividends, Capital gain from selling shares

- Tax:

- Dividends received from companies in the group will be exempted from 10% withholding tax and dividends received from affiliated companies will be exempted from corporate income tax.

- Capital gain: pay 20% corporate income tax and 0.1% stamp duty for share purchase agreement.

- Benefits: This strategy enhances the company’s appeal to the market by presenting both strong consolidated financial statements and business diversification.

- Considerations: When the IPO Holding Company sells shares, it is subject to a 20% corporate income tax, unlike individual shareholders who are exempt from capital gains tax.

อ่านบทความของเราในหัวข้ออื่นๆได้ที่นี่

สนใจสอบถามข้อมูลเพิ่มเติมเกี่ยวกับการจัดตั้งบริษัทโฮลดิ้ง Holding Company

หรืออยากนัดปรึกษากับเรา 📌 [ฟรี] 1 ชั่วโมงได้ที่ Google Calendar

อีเมล : Finniche.Planner@gmail.com

หรือกรอกแบบฟอร์มที่ Contact Us

ฟินนิช แพลนเนอร์ ที่ปรึกษาธุรกิจครอบครัว

#ที่ปรึกษาธุรกิจครอบครัว #ธุรกิจครอบครัว #FamilyHoldingCompany #โครงสร้างบริษัท #โครงสร้างผู้ถือหุ้น